Understanding Qualified Opportunity Zones

Qualified Opportunity Zones are areas selected by the government for revitalization efforts. Investing here not only offers the potential for tax deferral and reduction but also provides the chance to contribute to the development and improvement of these communities.

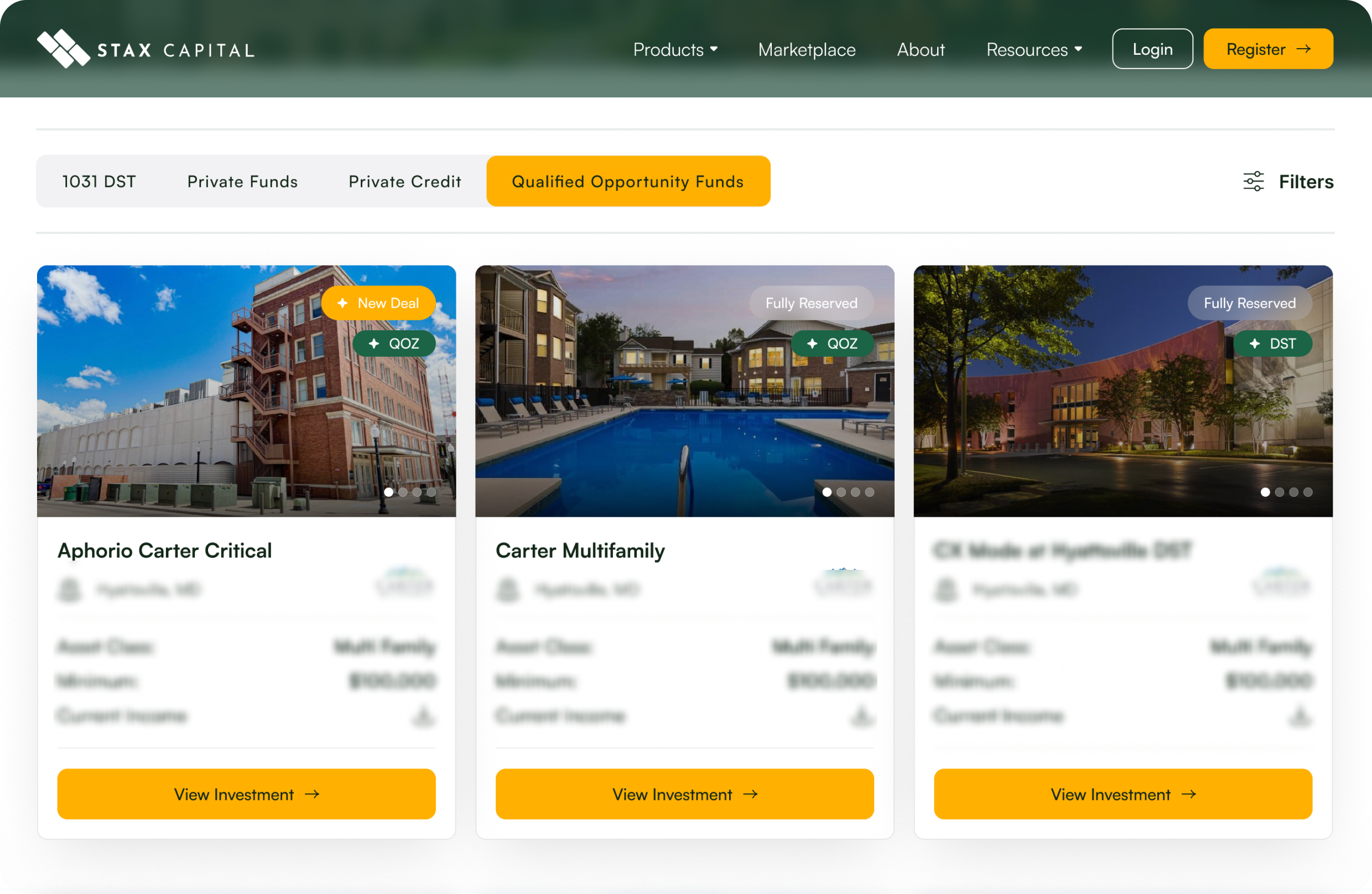

Featured Qualified Opportunity Funds

Explore our hand-picked Qualified Opportunity Funds to maximize your tax benefits while supporting economic development. Invest confidently, knowing your capital drives both financial growth and positive change.

Trilogy QOF Fund

- Asset Class: Multi Family

- Minimum: $100000

- Current Income No current income

Key Highlights

Optimized Tax Benefits: Our team helps you take full advantage of tax deferral and exemption opportunities under current QOF regulations. We do not however give tax advice and all investors considering a QOF should consult their tax advisor.

Carefully Vetted Opportunities: Each fund undergoes strict analysis to ensure you invest in opportunities backed by experienced managers.

Custom Portfolio Solutions: We work with you to design a QOF investment strategy tailored to your financial goals and risk tolerance.

Sponsor Assets Under Management

Real Estate offered on our platform

Highly-vetted investments from institutional DST managers

Access to a broad array of asset types

Maximize Benefits with Qualified Opportunity Funds

At Stax, we provide access to pre-vetted Qualified Opportunity Funds managed by industry leaders. You’ll benefit from a combination of tax savings, professional fund management, and the chance to invest in thriving industries.

Access unique QOF funds with experienced real estate sponsors.

Invest in key sectors through selected QOF funds, providing you with the potential to diversify and expand your investment reach.

Featuring Best in Class Fund Managers

Collaborate with some of the highly experienced in Class Fund Managers in the industry, ensuring professional management and effective strategies to managing your investments.

Exclusive Opportunities with Stax

Experience the advantage of working with Stax—where our deep expertise and tailored approach guide you in optimizing potential tax benefits of QOF investments.

Download the Complete QOZ Guide

Discover how investing in Qualified Opportunity Zones could enhance your portfolio while offering tax incentives. Download the guide to get started on your QOZ journey.

Download the Complete QOZ Guide

Discover how investing in Qualified Opportunity Zones could enhance your portfolio while offering tax incentives. Download the guide to get started on your QOZ journey.

QOZ Legislation

In 2017, the Tax Cuts and Jobs act established a new tax incentive to encourage investments in over 8,000 designated opportunity zones that haven't seen significant capital investment in decades.

When you invest in properties through qualified opportunity fund, you're not only eligible for significant tax benefits. You're also revitalizing up-and-coming communities by creating more jobs, driving business and expanding housing.

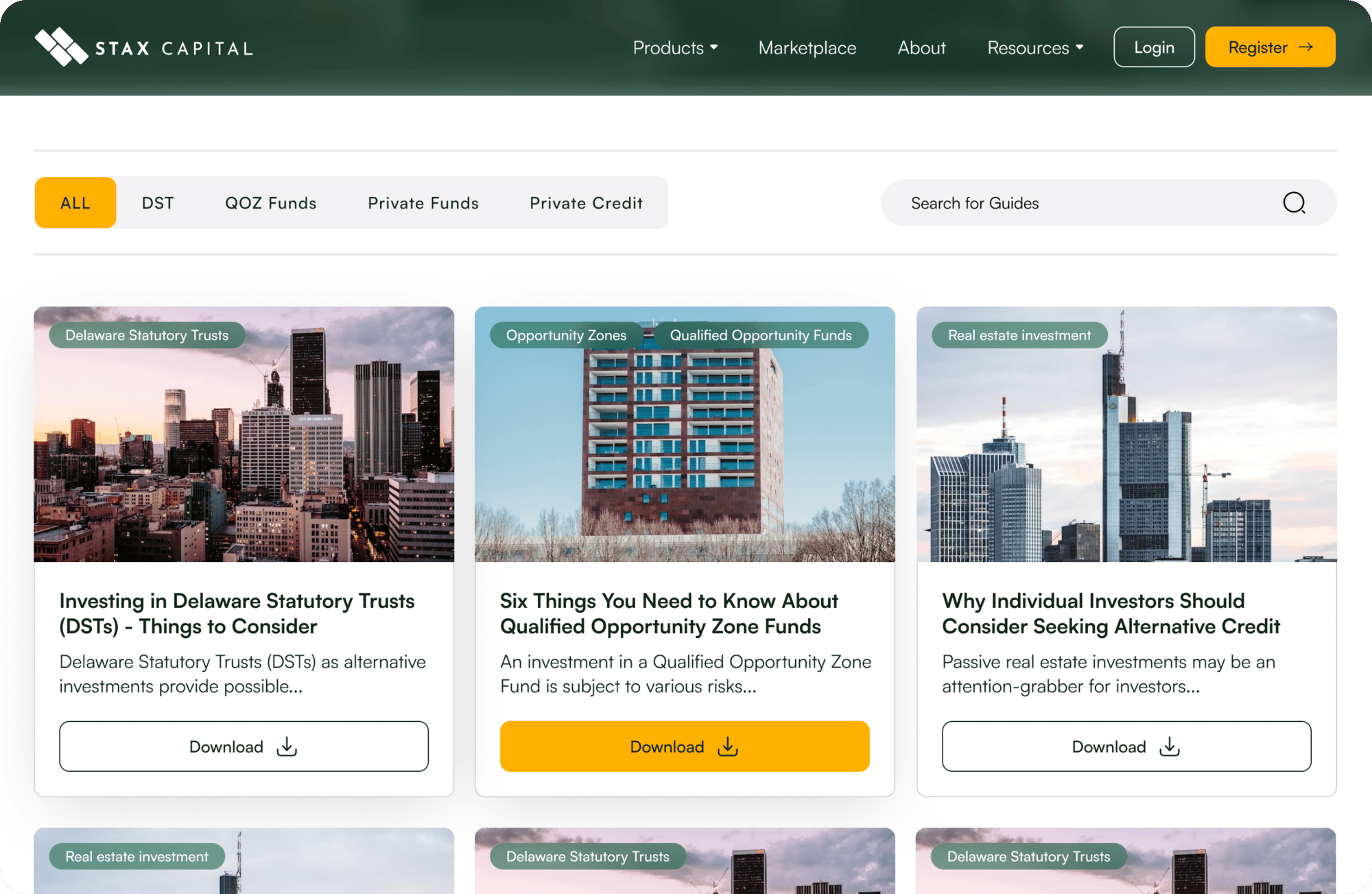

Market Insights

Gain access to our latest market insights with downloadable guides covering key trends, industry developments, and investment opportunities.

.png?width=826&height=502&name=Qualified%20Opportunity%20Funds%20A%20simple%20guide%20(1).png)

- Qualified Opportunity Funds

Qualified Opportunity Funds: A simple guide

An alternative option that can be explored by real estate investors looking to diversify their portfolio and take advantage of possible tax benefits is the Qualified Opportunity Zone investment opportunity. What is a Qualified Opportunity Fund? It’s a vehicle for investing in these zones, offering potential tax advantages. Here are some of the important things to know about investing in Qualified Opportunity Zones through Qualified Opportunity Funds.

Read More

%202021%20Update%20(1).png?width=826&height=502&name=Qualified%20Opportunity%20Funds%20(QOFs)%202021%20Update%20(1).png)

- Qualified Opportunity Funds

Qualified Opportunity Funds (QOFs): 2021 Update

One year after a global lockdown triggered by the COVID-19 outbreak

Read More

- Qualified Opportunity Funds

How to Defer and Eliminate Capital Gains Through QOZ Investments

Are taxes eating into your investment profits? What if you could delay or even avoid paying those taxes entirely? Qualified Opportunity Zones (QOZs) make this possible, giving investors a chance to defer and potentially eliminate capital gains taxes. However, these benefits come with specific IRS requirements and investment risks that should be carefully evaluated.

Read More

Case Stories

Explore firsthand experiences of clients who have successfully transitioned to passive income, built wealth, and diversified their portfolios with our guidance.

Stax made my transition to passive income smooth and stress-free.

Stax helped Shikha complete a 1031 exchange into DSTs, freeing her from property management and allowing her to focus on personal time.

-Shikha

Stax helped me shift to passive income and defer my taxes.

Stax guided Ramesh through a successful 1031 exchange and DST investments, allowing him to defer taxes and enjoy hassle-free income.

-Ramesh

Stax made it easy to switch to passive investments for our retirement.

Stax introduced Sima and Roman to DSTs, allowing them to shift from active property management to a hands-off strategy while maintaining a steady income.

-Sima and Roman

Disclosure

The experiences shared by clients of Stax Capital were given voluntarily without any compensation. These testimonials reflect individual opinions and are not intended as investment advice or guarantees of future results. Each investor should consider their own financial goals, risk comfort, and overall situation before making any investment choices.

Understanding the Benefits and Risks of Qualified Opportunity Funds

Unlock Powerful Tax Benefits and Understand the Potential Risks Involved in QOF Investments

Tax Deferral

Investing in a QOF within 180 days of a sale lets you defer capital gains taxes until the end of 2026. This gives you the time to reinvest and potentially expand your wealth without immediate tax implications.

Tax-free gains

By keeping your investment in a QOF for at least 10 years, you won’t need to pay taxes on the capital gains earned. This way you can increase your overall returns over the long term significantly.

Tax-Free Growth

QOFs offer the ability to keep your funds invested without additional capital gains tax until 2047. This gives you decades to potentially grow your wealth without capital gains taxes.

Diversified Opportunities

QOFs provide access to a variety of asset classes. This can further help balance your portfolio while spreading risk across different types of properties and sectors.

Speculative Investments

QOFs depend on market projections that may not materialize as expected. If these assumptions prove incorrect, it could lead to potential financial losses.

Illiquid Investment

There is no established market for QOF interests, making it difficult to sell or liquidate your investment. This means you need to be prepared for the long-term commitment.

Tax Risks

QOF tax rules can change, impacting the benefits you receive. Future changes could impact your investment returns and benefits, so staying informed about updates is important.

Regulatory Risk

The regulatory framework governing QOZ investing is still evolving. Future adjustments could impact your investment, and it’s important to stay informed about these changes.

Our Partners

Our network of industry-leading partners provides best-in-class investment managers, expert tax advisors, and solution-driven product developers. Together, we deliver exceptional investment solutions tailored to your needs.

Our Leadership Team

Our leadership team combines extensive knowledge of private markets with a shared dedication to putting clients first. We work closely with you, educating you on the pros and cons to ensure the decisions we help you make align with your long-term financial goals.

Founder & CEO

Founder & CEO

Stacey Morimoto

Due Diligence and Operations

Due Diligence and Operations

Quinn Morimoto

Compliance Principal

Compliance Principal

Jason Finley

Stacey Morimoto

Mr. Morimoto leverages over 20 years of experience in the securities industry to help his clients navigate the complexities of alternative investments.

After starting his career at Salomon Smith Barney and recognizing the limitations of the traditional wirehoue platform, Stacey became an independent financial representative and established his own securities broker dealer.

Through DST investments, he saw a unique opportunity to deliver real value to clients that larger firms couldn’t offer. The ability to improve the overall day-to-day quality of people’s lives, beyond just their finances, is still what drives him.

With Stax Capital, a boutique firm that prioritizes individual attention, Stacey’s mission is to deliver the best possible educational experience for investors, so that they can make the right decision for themselves.

Quinn Morimoto

Son of founder and CEO Mr. Stacey Morimoto, Quinn has benefitted from early exposure to the inner workings of the securities industry. With a degree in finance from the University of San Diego, he heads up the due diligence and underwriting for all the DST offerings brought to the Stax Platform, a process that includes gathering appraisals, third party reports, and legal opinions as well as recreating sponsors’ financial models. He dives deep into the numbers and analyzes offers from every angle, looking for flaws, in order to minimize as much risk as possible for investors. Quinn has directly facilitated hundreds of private placement investment transactions and would say that the best part of the job is being able to truly make a lasting impact on people’s lives.

Jason Finley

With two decades of experience in sales and marketing across prestigious golfing, technology, and non-profit sectors, Mr. Finley has consistently embraced roles centered on helping others. He firmly believes that enjoying your work makes it effortless, which is why he cherishes being part of the Stax Capital family.

Educating investors on often-overlooked investment opportunities to help them grow their wealth, achieve tax efficiency, and plan for the future brings him immense satisfaction. From the onboarding process to discussing investment options, Jason is dedicated to ensuring every client receives the highest level of service when working with Stax Capital.

Jason is a graduate of the FINRA Institute at Georgetown Certified Regulatory and Compliance Professional (CRCP) program, further enhancing his expertise and commitment to providing exceptional service and compliance in the financial sector. He also holds the Series 22, 7, and 24 securities licenses, underscoring his comprehensive knowledge and regulatory compliance proficiency.